Starting April 1st of this year, we replaced US small cap stock exposure in our active equities portfolios with US momentum stock exposure. We did this because small, fast-growing, vibrant companies are choosing to stay privately owned rather than publicly listing their shares. In addition, internet business models have created a “winner-take-all” dynamic in many segments of the economy. As a result, we believe momentum stock exposure is better than small company stock exposure for capturing returns during periods of low stock market stress. More details below.

Exploiting equity factors to capture maximum risk-adjusted returns for our clients is a core element of our investment approach. You can read more here on how we use factors in our portfolios.

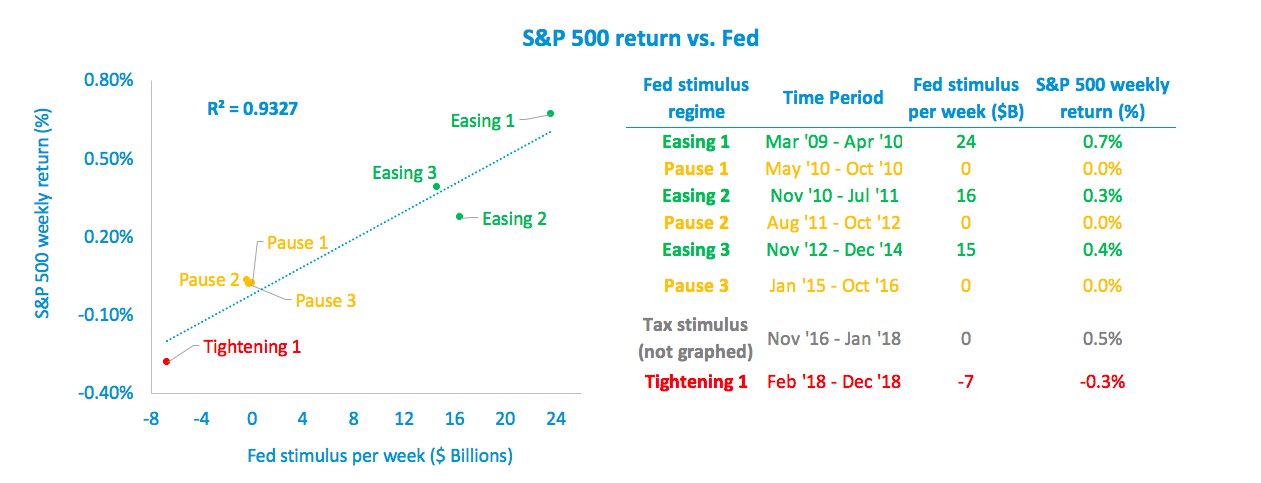

We originally designed our active equity portfolios to seek small cap US equity exposure via the Russell 2000 index ETF (IWM) in times of low equity market stress, as determined by our equity market stress indicator.

The relative outperformance of smaller companies over many decades has been heavily studied in the investing industry literature, and it has been generally attributed to small companies’ better growth opportunities combined with their comparative obscurity. If fewer investors have researched these companies, the rationale goes, there is better opportunity for a smart investor to buy their shares at a good price before other investors catch on.

Over the past few years, the strength of the small cap factor has been shown to be weakening - this Research Affiliates study and this Wall Street Journal article both give a nice overview.

Moreover, the U.S. equity market has changed dramatically in the past decade, and one of the biggest changes has been the shrinking population of publicly-traded small-cap companies - read more on that in this Vanguard research note. There are still plenty of small companies, they’re just not going public anymore to fund their growth - read more on that here. Instead, they’re choosing to stay privately held because they’re finding it easier to raise financing in the ever-expanding private capital market, as described in this McKinsey report. For an excellent first-hand account of this phenomenon, read “Why so few of our companies aspire to go public” by SSM Partners, a growth private equity firm focused on smaller companies.

In addition, the winner-take-all dynamic driven by companies like Amazon, Google, Netflix, and other internet-centric businesses, described in this New Yorker article, means that growth is accruing to fewer and fewer of the remaining publicly-traded companies. This dynamic favors ‘momentum’ companies – those whose recent stock price performance has been better than average.

The above chart shows how big the performance difference has been between small cap stocks and momentum stocks. In the past 5 years, the MSCI momentum stock index ETF (MTUM) has delivered nearly 2x the return of the broad S&P 500 index ETF, and nearly 3x the return of the Russell 2000 small cap index ETF.

Momentum companies’ outperformance relative to the broader population of publicly traded companies isn’t a new phenomenon. MSCI publishes the US momentum stock index that our portfolios use via the MTUM ETF, and their research shows this to have been true for decades. But momentum’s outperformance relative to small caps is stronger than ever, and we believe this will persist into the future.